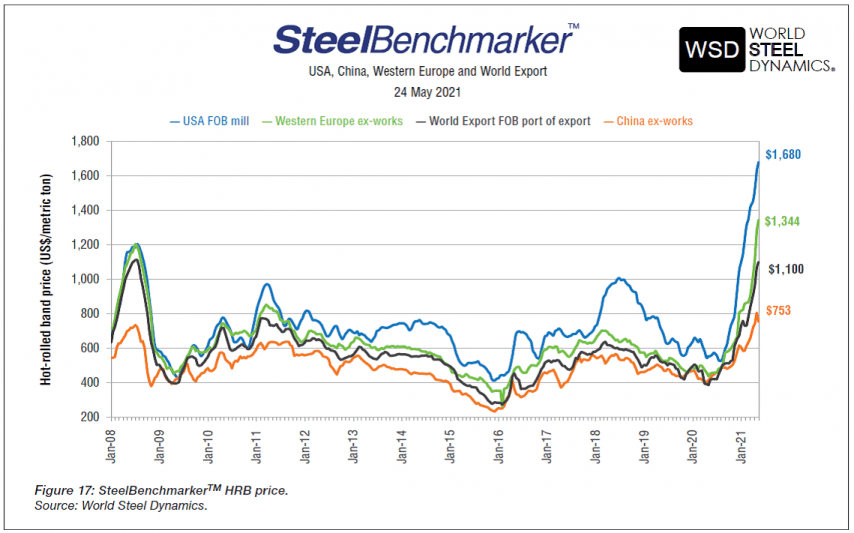

Global economies are on a path to recovery after a slump during the pandemic. This recovery continues to push the price of commodities high. The steel market has seen unprecedented fluctuation in pricing, with the trend likely to persist over the next year. Global politics, supply chain disruptions, fuel prices and heavy spending on infrastructure are factors that will continuously cause steel price swings.

The Australian market is no exception to the ever-volatile steel prices despite controlling more than 38% of the global iron ore production. The current price of iron ore is ~$150/tonne, with estimations that this price will drop further to ~$109/tonne by 2022. While western economies are pursuing economic growth through massive construction projects, China, the biggest importer of Australian iron ore, is slowing down investment in the property market. China, the largest steel producer in the world, is aiming to be carbon neutral by 2060. The Chinese government is putting measures to control steel production and reduce greenhouse gas emissions. It is a strategy that has seen annual steel production in China drop by 13.2% by August 2021. This decline significantly affects pricing dynamics across the world.

The COVID-19 pandemic saw some companies halting steel production leading to smaller inventories across the globe. At the same time, the demand for the product soared. As economies reopen, there is a higher demand for steel in heavy industries like automotive, machinery, oil and gas. Manufacturers are walking a tightrope as they try to rebuild steel inventories and satisfy demand. In general, World Steel Association (WSA) reports a 1.4% year-on-year increase in steel production for the period ending in August 2021.

Supply Chain Interruptions

The pandemic period has been a wake-up call for global economies. Geopolitics, scarcity of products and trade wars spelled doom to previously sustainable supply chains. The shortage of shipping containers, protracted delays in deliveries and trade sanctions like the one between Australia and China in May 2020 slowed down steel production and distribution throughout the world. Supply chain interruption means that steel producers globally are struggling to restore operations to normal levels.

As supply chain interruptions persist, the overall cost of steel transportation keeps rising. Manufacturers pass down these costs to consumers, propelling the global prices of steel in all its alloys to record high levels.

Australian Steel Market Overview

The Australian economy is steadily rebounding. Amid this recovery is a serious concern over the rising cost of steel. The government has set out an ambitious project that aims to boost the local manufacturing sector, a strategy that has attracted more local investors. Agriculture is another sector that has seen tremendous growth over the past year across the country.

The progress of these economic sectors is accompanied by massive construction. Local manufacturers are expanding their production and warehousing facilities. Massive investment in infrastructure projects and the minerals technology industries are also driving demand for steel throughout Australia.

Where Does the Steel Industry Go From Here?

Whilst the industry has enjoyed relatively stable pricing in the decade prior to 2021, steel is like any other commodity – subject to fluctuations due to demand, raw material availability, shipping costs, and uniquely, the myriad disruptions caused by a once in a lifetime pandemic.. Whilst supply chains are returning to normalcy this does not guarantee that the prices will stop fluctuating. When setting the prices of commodities, industry players rely heavily on data from manufacturing supply chains. It is a reactive pricing strategy that has had its successes in the past. The pandemic and post-pandemic periods have tested this strategy to the limits. As it stands, steel manufacturers and businesses need to re-think their pricing models to avert business losses and cushion customers from high prices to ensure a sustainable and supply.

The operations in steel manufacturing industries around the globe are returning to normalcy. Iron ore prices globally are yet to stabilize. There are expectations that steel pricing will plateau in the last half of 2022, however with multiple factors influencing the costs, this is speculation only.

Lessons for Businesses in the Steel Sector

It has been a rough few years for businesses with volatile steel prices leading to financial losses. Price fluctuations have had far-reaching consequences across all sectors of the economy. As we move forward, players in the steel sector should adopt digital tools and technology to generate accurate demand forecasts, optimize pricing and scale up operations to match actual market demands. Companies must adapt quickly to market dynamics and leverage data to counter volatilities. By using appropriate technologies, steel manufacturers can segment the consumer market and optimize pricing for every segment.

Is there an end in sight? Definitely yes — On the condition that steel industry players adapt quickly to the ever-changing market dynamics.

Join the pipeline

Our quarterly update on industry news,

cutting edge products, and key insights.

AG630

AG630 AG631

AG631 AG632

AG632 AG634

AG634 AG636

AG636 AG100

AG100 AG110

AG110 AG112

AG112 AG115

AG115 AG120

AG120 AG130

AG130 AG150

AG150 AG160

AG160 AG170

AG170 AG190

AG190 AG200

AG200 AG220

AG220 AG250

AG250 AG260

AG260 AG550

AG550 AG560

AG560 AG565

AG565 AG570

AG570 AG580

AG580 AG585

AG585 AG590

AG590 AG595

AG595 AG620

AG620 AG412

AG412 AG415

AG415 AG420

AG420 AG430

AG430 AG435

AG435 AG440

AG440 AG445

AG445 AG470

AG470 AG475

AG475 AG480

AG480 AG485

AG485 AG490

AG490 AG495

AG495 AG510

AG510 AG515

AG515 AG530

AG530 AG270

AG270 AG280

AG280 AG290

AG290 AG295

AG295 AG300

AG300 AG310

AG310 AG320

AG320 AG330

AG330 AG340

AG340 AG350

AG350 AG360

AG360 AG370

AG370 AG385

AG385